New Year Tax and Payroll Changes for 2024-25

New Year Legislation and Changes from the Spring Budget for the 2024-25 tax year. From 6 April 2024 to 5 April 2025, these figures are in effect:

PAYE Tax and National Insurance Contributions

The standard employee personal allowance for the 2024 to 2025 tax year is:

- £242 per week

- £1,048 per month

- £12,570 per year

Tax Thresholds, Rates, and Codes

- Deductions depend on employees’ tax codes and income exceeding their Personal Allowance.

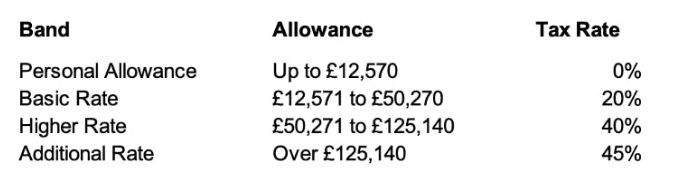

Tax bands and rates in England, Northern Ireland and Wales

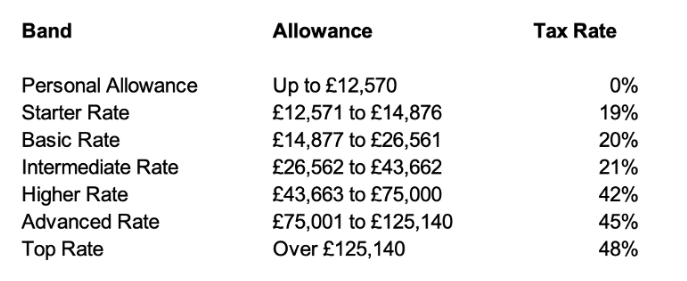

Tax bands and rates for Scotland

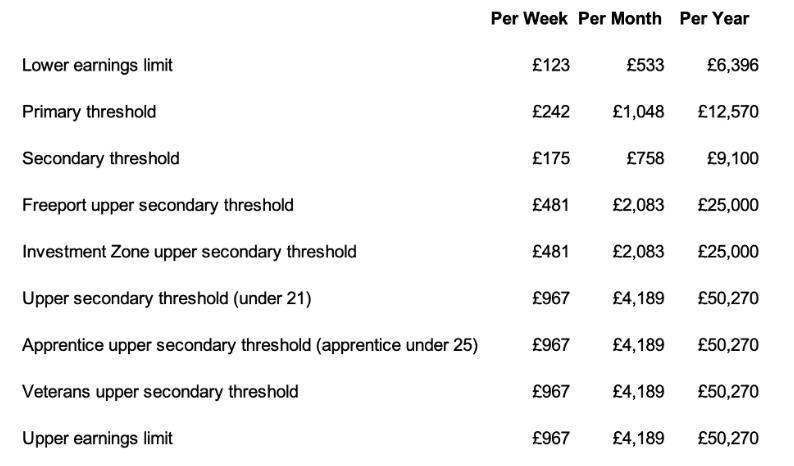

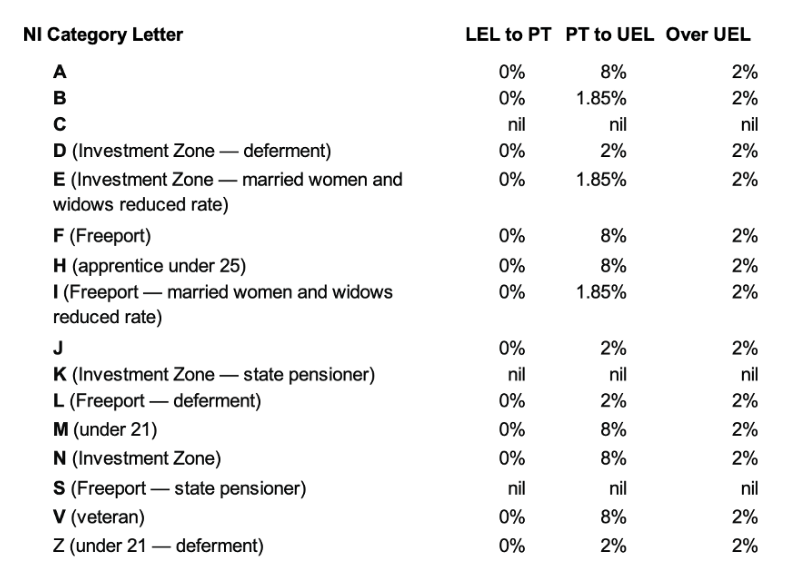

Class 1 National Insurance Thresholds and Rates

- Deductions apply to earnings above specified thresholds – see below.

- Rates vary based on earnings and specific categories.

National Employee primary contribution rates

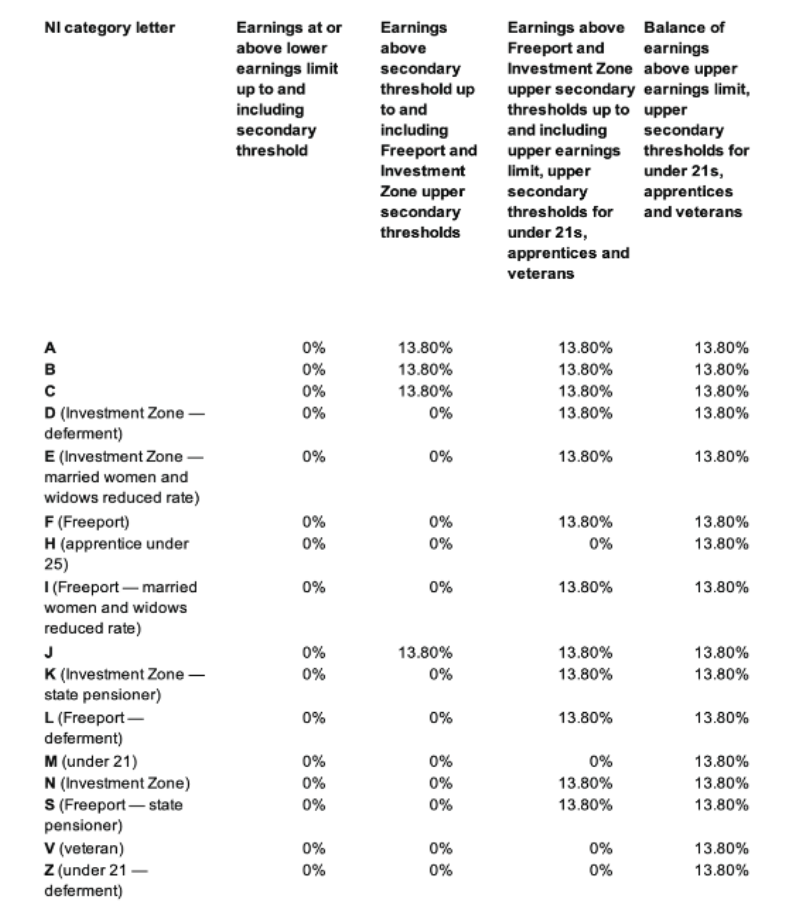

Class 1A National Insurance: Expenses and Benefits

- Pay Class 1A National Insurance on work benefits given to employees.

- The rate for 2024 to 2025 is 13.8%.

Employer (secondary) contribution rates

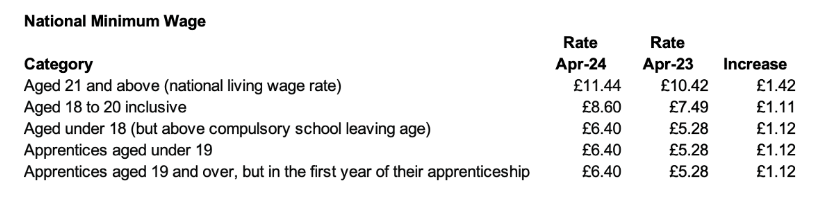

National Minimum Wage

Automatic enrolment

The thresholds for the 2024/2025 remain the same as the previous three tax years.

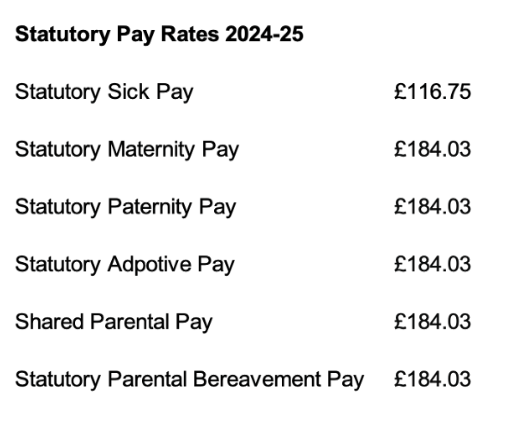

New Statutory Rates: Statutory Maternity, Paternity, Adoption, Shared Parental, and Parental Bereavement Pay

- Rates and conditions for these payments apply from 7 April 2024.

The new Statutory Sick Pay rate is applicable from 6th April 2024 and the new parental statutory pay rates are applicable from the first Sunday in the new tax year – 7th April 2024.

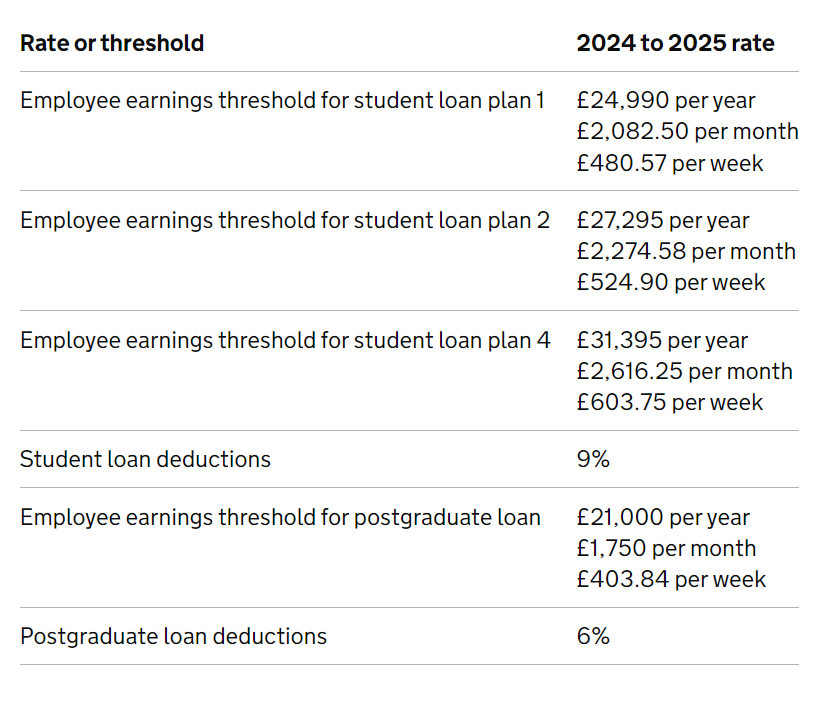

Student Loan and Postgraduate Loan Recovery

- Record and deduct repayments if earnings exceed thresholds.

- Rates and thresholds vary for different loan plans.

Company Cars: Advisory Fuel Rates

- Use advisory rates for mileage costs if providing company cars.

- Rates differ based on engine size and fuel type.

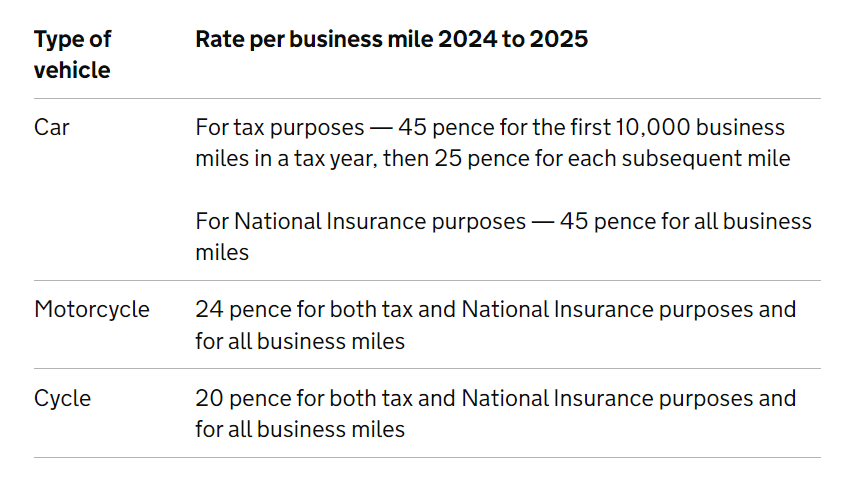

Employee Vehicles: Mileage Allowance Payments

- Pay employees for business mileage without reporting to HMRC.

Employment Allowance

- Eligible employers can reduce National Insurance liability by up to £5,000 annually.

Apprenticeship Levy

- Charged at 0.5% of the annual pay bill for employers with a total bill exceeding £3 million.

- An allowance of £15,000 is available to offset the levy.

For more information on the New Year changes, please visit HMRC’s website: https://www.gov.uk/guidance/rates-and-thresholds-for-employers-2024-to-2025

These changes are now live in Capium.